What Is Source Code Escrow and How It Protects NBFCs from Vendor Failure

Apr 01, 2026

What Is Source Code Escrow and How It Protects NBFCs from Vendor Failure

Source code escrow is a structured continuity mechanism that allows an NBFC to access and use critical software if its technology vendor becomes unavailable. It protects NBFCs by ensuring access to source code under predefined trigger conditions, reducing dependency on a single provider and preserving operational control during vendor failure.

In regulated financial environments, escrow is not just a legal arrangement—it is a continuity safeguard.

For regulatory context, see our detailed guide on RBI mandates on software continuity.

Table of Contents

What Is Source Code Escrow?

Why Vendor Failure Is a Serious Risk for NBFCs

How Source Code Escrow Protects NBFCs in Practice

When Is Source Code Escrow Triggered?

Why Contracts and SLAs Alone Are Not Enough

How Escrow Aligns with Regulatory Expectations

Where SprintEX-Code Fits In

Summary Table

Conclusion

Frequently Asked Questions (FAQs)

What Is Source Code Escrow?

Source code escrow is an arrangement where a software vendor deposits the application’s source code with an independent third party. The code remains protected during normal operations and is released only if defined trigger events occur.

Escrow does not transfer ownership during normal business activity.

Its purpose is to ensure recoverability if vendor dependency turns into operational risk.

However, depositing code alone does not automatically guarantee usability. The risks of unverified deposits are explored in why deposited code does not always ensure continuity.

Why Vendor Failure Is a Serious Risk for NBFCs

NBFCs rely heavily on third-party software providers for:

Loan origination and loan management systems

Customer and transaction databases

Compliance and regulatory reporting tools

Financial processing infrastructure

Under normal conditions, these systems operate seamlessly. Risk becomes visible only when vendor stability is disrupted.

Vendor failure may result from insolvency, acquisition, internal disputes, restructuring, or prolonged service breakdown.

The most serious risk is not temporary downtime—it is loss of control over the software itself.

Without access to source code, an NBFC may be unable to:

Fix defects or security issues

Implement regulatory updates

Migrate to an alternate provider

Maintain operational continuity

A step-by-step breakdown of what typically fails during vendor exits is detailed in what actually breaks during a vendor exit.

How Source Code Escrow Protects NBFCs in Practice

When properly structured, source code escrow creates a controlled safeguard that activates only when necessary.

It protects NBFCs by:

Guaranteeing access to source code during vendor failure

Enabling maintenance through internal teams or alternate providers

Reducing single-vendor concentration risk

Supporting structured recovery under defined conditions

Escrow is preventive. It ensures continuity options exist before disruption occurs.

The difference between storage-only escrow and release-ready escrow is explored in release-ready vs storage-only escrow.

When Is Source Code Escrow Triggered?

Escrow agreements define specific release conditions. These typically include:

Vendor insolvency or liquidation

Cessation of software support

Prolonged service outages

Material breach of maintenance obligations

Triggers are structured to balance:

Protection of vendor intellectual property during normal operations

Timely access for the NBFC when continuity is genuinely at risk

This balance supports both commercial fairness and operational resilience.

Why Contracts and SLAs Alone Are Not Enough

Contracts and service-level agreements define legal rights. They are necessary—but insufficient.

Contracts provide legal remedies.

Escrow provides technical recoverability.

If a vendor fails suddenly, enforcing contractual rights does not restore systems in real time. Escrow addresses the technical layer of risk.

In regulated financial environments, continuity is assessed based on operational outcomes—not contractual documentation.

How Escrow Aligns with Regulatory Expectations

Regulators emphasize:

Third-party risk management

Operational resilience

Control over outsourced technology

Demonstrable recoverability

While escrow may not always be explicitly mandated, regulators expect NBFCs to show that critical systems can be controlled even if vendors fail.

Escrow supports this by converting vendor dependency into a structured fallback mechanism.

For a product-focused implementation perspective, see how SprintEX-Code supports RBI continuity expectations.

Where SprintEX-Code Fits In

Modern escrow solutions such as SprintEX-Code by PaySprint are designed specifically for regulated financial institutions.

Rather than functioning as passive storage, SprintEX-Code emphasizes:

Verified and usable code deposits

Clearly defined trigger mechanisms

Governance-aligned documentation

Operational readiness for recovery scenarios

This positions escrow as an operational control—not merely a legal safeguard.

Summary: Vendor Failure With vs Without Escrow

Conclusion

Source code escrow protects NBFCs from vendor failure by ensuring controlled access to critical software under predefined conditions. It reduces dependency on single providers and strengthens operational resilience during disruption.

As financial systems become increasingly software-driven, vendor risk becomes continuity risk.

Escrow transforms that risk into a structured and executable safeguard.

In regulated financial environments, continuity is not optional—it is a governance responsibility.

Frequently Asked Questions (FAQs)

What exactly is source code escrow?

Source code escrow is an arrangement where a vendor deposits application source code with an independent third party, ensuring the customer can access it under defined failure conditions.

Why do NBFCs need source code escrow?

NBFCs rely on third-party software for critical operations. Escrow protects them from losing control if a vendor becomes insolvent or stops providing support.

What happens if a vendor fails without escrow?

Without escrow, an NBFC may lose the ability to maintain, modify, or migrate its software—leading to operational and regulatory risk.

When is source code released from escrow?

Release occurs only under predefined triggers such as insolvency, prolonged service disruption, or breach of support obligations.

Does escrow replace contracts or SLAs?

No. Contracts provide legal protection. Escrow ensures technical continuity. Both address different layers of risk.

Is source code escrow relevant for regulatory compliance?

Yes. While not always mandated by name, escrow supports expectations around operational resilience, third-party risk management, and continuity planning.

Related Posts

What is E-Banking? Meaning, Types, Benefits & How It Works in India.

E-banking is the digital way of accessing banking services through mobile apps, websites, ATMs, and biometric systems. It enables secure, fast, and branchless financial transactions anytime and anywhere in India.

Read More

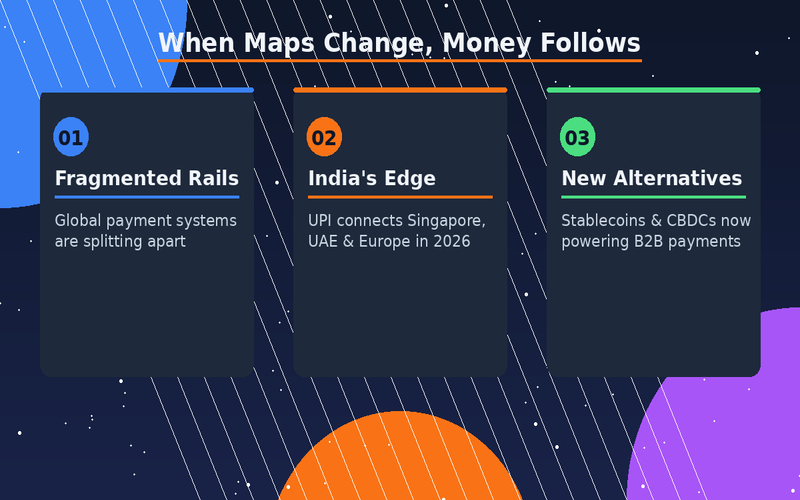

When Maps Change, Money Follows: How Geopolitics Is Rewiring B2B Payments in 2026

Payments are no longer just a plumbing problem — they're a geopolitical one. Explore how Indian B2B businesses can navigate a fragmented, fast-changing global payment landscape

Read More

What Happens Inside an Escrow Release Event? A Step-by-Step Breakdown for Businesses

A complete breakdown of escrow release events—covering triggers, validation, vendor response, and access to source code—helping businesses ensure continuity and minimize vendor risk.

Read MoreReady to Protect Your Core Systems?

Join enterprises that trust SprintEX-Code to safeguard their mission-critical software. Get started with a consultation to discuss your specific escrow requirements.