Escrow API Guide for Fintechs

Jul 09, 2026

Escrow API Integration Guide: How to Add Escrow Infrastructure to Your Fintech Product

An escrow API is what turns a regulated escrow account from a slow, manual bank process into something a fintech can plug into its product in weeks. It's the layer that lets your backend programmatically create escrow instances, hold funds, set release conditions, and trigger disbursements — without your team having to chase bank officers or reconcile spreadsheets by hand.

Most content on this topic stays conceptual — explaining that "APIs are transforming escrow banking" without ever showing what integration actually looks like. This guide is different. It's a practical, step-by-step breakdown of what an escrow API integration involves, using PaySprint's SprintEXcrow as the reference implementation, since it's built specifically as an API-first escrow infrastructure layer for the Indian market.

Table of Contents:

What SprintEXcrow's Escrow API Actually Does

Integration Timeline at a Glance

Escrow API vs Payment Gateway API

Common Integration Mistakes to Avoid

Escrow API Use Cases by Industry

Security & Compliance Checklist for Escrow API Integration

Conclusion

Frequently Asked Questions

What SprintEXcrow's Escrow API Actually Does

Account/instance creation — programmatically spins up a new escrow account or sub-account per transaction, buyer-seller pair, or project

Fund-in / deposit webhook — pushes a real-time notification the moment funds land, so you're not polling for status

Condition/milestone configuration — defines release rules: single approval, multi-party sign-off, time-based trigger, or external verification (KYC, delivery confirmation, milestone sign-off)

Release/disbursement API — triggers fund release once conditions are met, including split disbursements (commission deduction, TDS, multi-vendor payouts)

Reconciliation & reporting API — pulls transaction-level data for finance teams and regulatory audit trails

Refund/reversal API — handles the failure path: disputes, cancelled orders, or unmet conditions

Integration Timeline at a Glance

Escrow API vs Payment Gateway API

Common Integration Mistakes to Avoid

Treating escrow like a payment gateway — release logic is conditional, not instant; product logic built around synchronous checkout flows will need rework

Skipping the sandbox phase — partial releases, refunds, and multi-party disputes should be tested before production

Underestimating compliance review time — for regulated verticals, trustee sign-off is usually the longest step, not the code

Ignoring webhook idempotency — fund-in and release events must be handled idempotently so a duplicate webhook can't trigger a duplicate disbursement

Bolting on reconciliation after launch — audit-trail and reporting needs are far cheaper to design in from day one

Escrow API Use Cases by Industry

Security & Compliance Checklist for Escrow API Integration

Data encryption — confirm TLS in transit and encryption at rest for transaction data

RBI/SEBI/RERA alignment — verify the escrow structure matches your vertical's specific regulatory mandate

Trustee oversight — check that a licensed trustee governs fund release, not just the API layer

Access control — role-based permissions for who can configure release conditions or trigger disbursement

Audit trail immutability — reconciliation records should be tamper-evident for regulator review

Data localization — confirm transaction data is stored in compliance with Indian data residency norms

Conclusion

An escrow API integration isn't fundamentally different from integrating any other regulated financial infrastructure — but its conditional, webhook-driven nature demands different architectural assumptions than a payment gateway. Scoping for webhooks, idempotency, and compliance review time upfront — rather than treating it as "just another API" — is what separates a smooth 6-week build from a stalled one. PaySprint's SprintEXcrow is built API-first specifically to shorten that path for Indian fintechs, NBFCs, marketplaces, and lending platforms.

Frequently Asked Questions

Q1.How much does escrow API integration cost?

Escrow API integration is free to set up — no upfront fees, sandbox included.

Escrow API charges per transaction, roughly 0.7–0.89% of transaction value.

Escrow API costs more via custom pricing for real estate/lending platforms.

Q2. Is escrow API pricing based on transactions or a flat monthly fee?

Escrow API pricing is transaction-based, not flat — roughly 0.7–0.89% per transaction.

Escrow API has no subscription fee for standard use.

Escrow API flat fees only appear in enterprise real estate/lending deals.

Q3. Are there setup costs for accessing the escrow API?

Escrow API access has no setup fee for standard use — you only pay a per-transaction fee once live.

Q4.Does escrow API pricing vary by industry (lending, real estate, e-commerce)?

Escrow API pricing does vary by industry — e-commerce uses transparent per-transaction rates, while lending and real estate rely on custom, enterprise-negotiated pricing.

Q5. Is there a free tier or sandbox-only plan for escrow APIs?

Yes — Escrow API providers like Escrow.com offer a free sandbox environment for testing and integration, with no cost until you go live and start processing real transactions.

Related Posts

What is E-Banking? Meaning, Types, Benefits & How It Works in India.

E-banking is the digital way of accessing banking services through mobile apps, websites, ATMs, and biometric systems. It enables secure, fast, and branchless financial transactions anytime and anywhere in India.

Read More

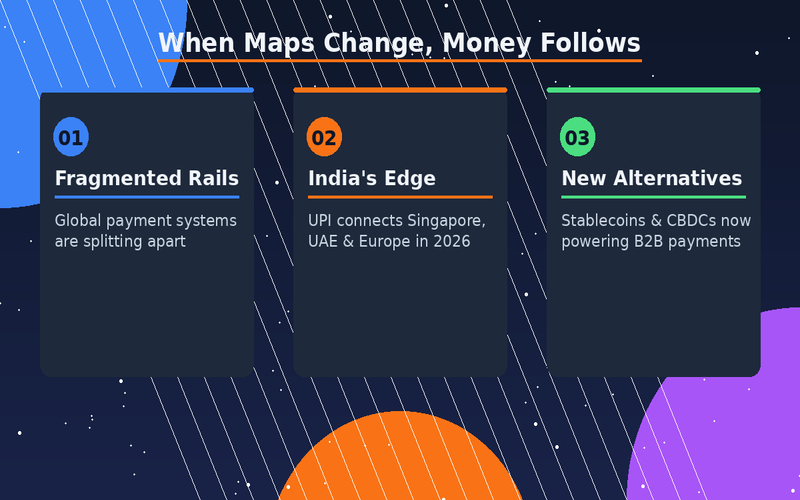

When Maps Change, Money Follows: How Geopolitics Is Rewiring B2B Payments in 2026

Payments are no longer just a plumbing problem — they're a geopolitical one. Explore how Indian B2B businesses can navigate a fragmented, fast-changing global payment landscape

Read More

What Happens Inside an Escrow Release Event? A Step-by-Step Breakdown for Businesses

A complete breakdown of escrow release events—covering triggers, validation, vendor response, and access to source code—helping businesses ensure continuity and minimize vendor risk.

Read MoreReady to Protect Your Core Systems?

Join enterprises that trust SprintEX-Code to safeguard their mission-critical software. Get started with a consultation to discuss your specific escrow requirements.