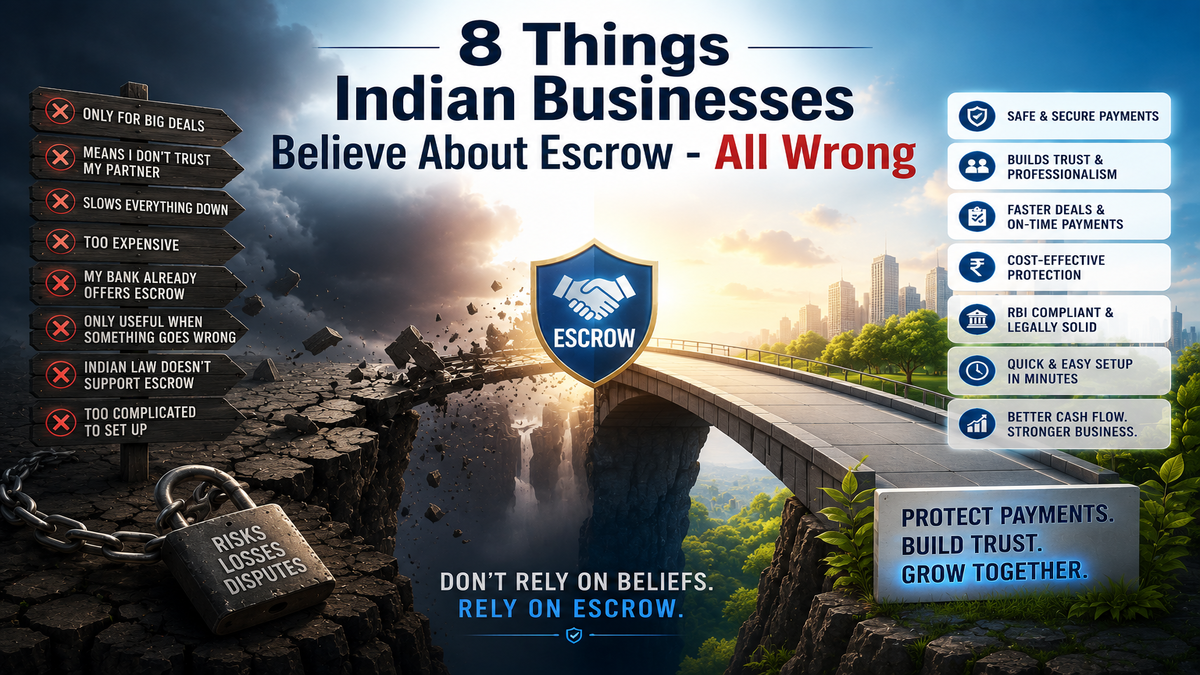

8 Things Indian Businesses Believe About Escrow — All Wrong

May 12, 2026

8 Things Indian Businesses Believe About Escrow - All Wrong

Here is a sentence that has cost Indian businesses thousands of crores:

"We don't need Escrow - we trust each other."

Trust is not a payment mechanism. Trust doesn't release funds when goods arrive. Trust doesn't hold a buyer accountable when they pay 40% less than agreed. Trust doesn't stop a supplier from disappearing after taking an advance. Most of B2B India still operates on a handshake and a wire transfer — because escrow is widely misunderstood. It's seen as complex, expensive, offensive, or irrelevant. Every one of those beliefs is wrong. Here's the proof: Rs.1.5L Cr+ lost annually to B2B payment defaults in India. 7 in 10 SMEs have experienced at least one payment dispute.

Table of Content

The 8 Myths About Escrow in India

All 8 Myths at a glance

The 8 Myths about Escrow in India

MYTH #1 "Escrow is only for big companies and large deals."

REALITY: Escrow is for any business that wants to get paid — or pay safely.

This is perhaps the most damaging myth. It was born in an era when escrow required lawyers, trust accounts, and weeks of paperwork. That era is over.

Escrow is built for the Rs.50,000 deal between a Pune manufacturer and a Delhi distributor. For the Rs.2 lakh advance a startup needs to pay a new logistics partner. For the Rs.15 lakh transaction between a marketplace and a first-time seller.

There is no minimum deal size. No enterprise contract required. Any KYB-verified business can open an escrow transaction in minutes.

MYTH #2 "Using escrow means I don't trust my business partner."

REALITY: Using escrow means both parties are protected — not accused.

This is the most emotionally loaded myth, and it stops more deals from being protected than any other.

Think about it differently. When you sign a contract, are you saying you don't trust the other party? Of course not. A contract is simply a shared record of what was agreed. Escrow is the same - but for the money itself.

Suggesting escrow is now widely understood as a sign of professionalism. It tells your counterpart: I take this deal seriously. I want both of us protected. That's not distrust. That's respect.

The businesses that resist escrow aren't the trustworthy ones. They're often the ones who benefit from ambiguity.

MYTH #3 "Escrow slows everything down."

REALITY: Escrow speeds up decision-making - and releases funds the same day conditions are met.

Adding a third party sounds like adding a step. But consider what 'fast' actually looks like without escrow:

Without escrow, a wire transfer takes 2 minutes - but you spend 3 weeks following up, and if a dispute opens, you're dealing with lawyers. Payment might arrive 90–120 days late.

With SprintEXcrow, funds are locked in 5 minutes. Conditions are defined upfront - no follow-up needed. Disputes are resolved within days. Payment is released the same day delivery is confirmed.

The 2-minute wire transfer that takes 90 days to actually result in payment is not fast. It's deferred pain.

MYTH #4 "Escrow is expensive. The fees aren't worth it."

REALITY: The cost of escrow is a fraction of what a single dispute costs you.

Let's run the numbers. A legal dispute alone costs Rs.15,000 – Rs.80,000 in fees. A payment default can cost Rs.2L – Rs.10L per incident. And you might spend 3 to 7 months chasing overdue payments.

SprintEXcrow's fee? A small fraction of 1% of the transaction value. For a Rs.5 lakh deal, it costs less than a single round of courier-and-lawyer correspondence.

The question isn't whether escrow is affordable. The question is whether you can afford not to use it.

MYTH #5 "My bank already offers escrow. I don't need a separate platform."

REALITY: Bank escrow and platform escrow are fundamentally different products.

Most Indian banks do offer escrow accounts — for real estate transactions, typically above Rs.50 lakh, requiring branch visits and weeks of documentation.

SprintEXcrow is designed for B2B commerce at any size. It's 100% digital — KYB verification takes under 10 minutes. Funds release automatically when milestones are met. There's a built-in dispute resolution layer. And it's API-ready for marketplace operators.

If your bank's escrow worked for your B2B transactions, you wouldn't have payment disputes. The data says otherwise.

MYTH #6 "Escrow is only useful when something goes wrong."

REALITY: Escrow prevents things from going wrong in the first place.

This is like saying a seatbelt is only useful when you crash. True — but also exactly backwards.

The presence of escrow changes behaviour before the transaction begins:

The buyer knows their money is committed — no more vague 'I'll transfer by end of week.' The funds are already locked.

The supplier knows the money exists. They deliver with confidence instead of anxiety.

The terms are documented. Both parties agreed before a single rupee moved. There's no room for 'that's not what we discussed' later.

Escrow doesn't just protect you when something breaks. It changes the entire dynamic so fewer things break.

MYTH #7 "Indian law doesn't really support escrow. It's legally risky."

REALITY: SprintEscrow operates on fully RBI-compliant infrastructure. It is legally solid.

This myth likely comes from confusion between informal escrow arrangements and regulated escrow infrastructure. Informal escrow — where a friend or lawyer 'holds' money - is indeed legally murky.

SprintEXcrow is different. It is built on RBI-compliant payment rails, with full KYB verification and documented release conditions. Every transaction is traceable, auditable, and enforceable under Indian law.

In fact, using SprintEXcrow gives you stronger legal standing in a dispute than a standard wire transfer — because the release conditions, the parties, and the timeline are all recorded before the transaction begins.

MYTH #8 "Setting up escrow is too complicated. We don't have time for this."

REALITY: KYB verification takes under 10 minutes. Your first transaction can go live the same day.

Here's how simple it actually is:

Step 1: Sign up and submit KYB documents — under 10 minutes.

Step 2: KYB verification — same business day.

Step 3: Create your first escrow transaction — under 5 minutes.

Step 4: Counterparty accepts terms — minutes to hours.

Step 5: Funds locked, deal begins — instant.

Total setup time for your first protected transaction: less than half a day. Total time spent chasing payment disputes without escrow: months.

All 8 Myths at a Glance

Print this. Share it with your finance team. The next time someone says one of these things in a meeting, you'll know exactly what to say.

Conclusion

The most expensive word in Indian B2B isn't a fraud. It isn't a bad contract. It isn't even a rogue supplier. It's the word 'later.'

As in: 'We'll sort out the payment later.' As in: 'Let's not complicate things with escrow, we trust each other.' Every myth in this article is a version of 'later.' And later always costs more than now.

SprintEXcrow exists for businesses that have decided to stop paying the 'later' tax. The setup is fast, the cost is minimal, and the protection is total. The only thing left is the decision.

Stop believing the myths. Start protecting the money.

Frequently Asked Questions

Q1. Is escrow legally valid for small B2B transactions in India?

Yes. SprintEXcrow is built on fully RBI-compliant infrastructure. All transactions are legally traceable and enforceable regardless of deal size.

Q2. What types of businesses can use SprintEscrow?

Any KYB-verified business — from a sole proprietor to a large enterprise. Manufacturers, distributors, logistics providers, marketplaces, service companies, and platform operators all use it.

Q3. Can escrow work for service-based transactions, not just physical goods?

Yes. Milestone escrow is particularly well-suited for services — funds are released in tranches as each deliverable or project milestone is verified, protecting both sides throughout the engagement.

Q4. How are disputes handled inside SprintEXcrow?

A built-in dispute resolution window keeps funds frozen while both parties present their case. The platform enforces pre-agreed conditions as the basis for resolution — no lawyers required for most cases.

Q5. What happens if the counterparty refuses to use escrow?

That itself is important information. A legitimate business with nothing to hide has no reason to avoid a neutral payment hold. Resistance to escrow is often the first red flag in a transaction.

Q6. Does SprintEXcrow integrate with existing systems?

SprintEXcrow offers a developer-ready API for platform and marketplace integration. For individual business use, the web interface handles all transaction management without any integration needed.

Related Posts

What is E-Banking? Meaning, Types, Benefits & How It Works in India.

E-banking is the digital way of accessing banking services through mobile apps, websites, ATMs, and biometric systems. It enables secure, fast, and branchless financial transactions anytime and anywhere in India.

Read More

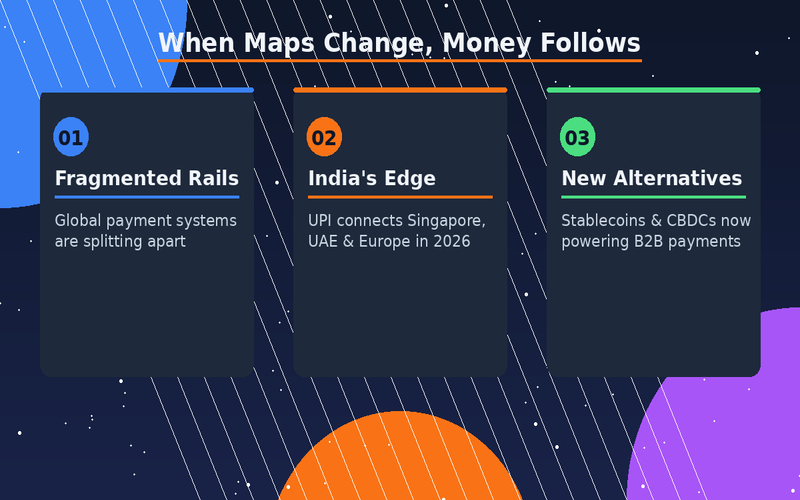

When Maps Change, Money Follows: How Geopolitics Is Rewiring B2B Payments in 2026

Payments are no longer just a plumbing problem — they're a geopolitical one. Explore how Indian B2B businesses can navigate a fragmented, fast-changing global payment landscape

Read More

What Happens Inside an Escrow Release Event? A Step-by-Step Breakdown for Businesses

A complete breakdown of escrow release events—covering triggers, validation, vendor response, and access to source code—helping businesses ensure continuity and minimize vendor risk.

Read MoreReady to Protect Your Core Systems?

Join enterprises that trust SprintEX-Code to safeguard their mission-critical software. Get started with a consultation to discuss your specific escrow requirements.